Trends in the display industry are heavily influenced by the developments in the consumer electronics markets, and this is seen in the rapid growth of the OLED panel market due to the rising demand from smartphone and TV brands. In its recent analyses of the panel market by technology, WitsView, a division of TrendForce, finds that the market share of OLED in the small size bracket continues to grow at the expense of LCD’s market share. Furthermore, WitsView anticipates OLED’s representation in the smartphone market will increase substantially following the release of iPhone X. With Apple expected to support this display technology in the future, the percentage of OLED models in the total annual smartphone shipments worldwide is projected to climb from 28% this year to 33% in 2018.

|

|

(Image: Apple) |

On the other hand, OLED panels, especially flexible ones, remain in scarce supply and will be exclusive to a small number of smartphone brands. Besides the rising OLED demand, device makers are also making the shift to the 18:9 screen aspect ratio. “Compared with flexible OLED panels, the market penetration of full-screen format will be much quicker” said Eric Chiou, research vice president of WitsView. “The rapid adoption of the 18:9 format is expected to take place across the market segments, from the premium to the mid-range and even the entry-level models.”

Based on WitsView’s latest projection, models featuring 18:9 screens are going to make up 9.6% of this year’s total smartphone shipments worldwide. This penetration rate will then soar next year, coming to around 36.2% of the global annual shipments.

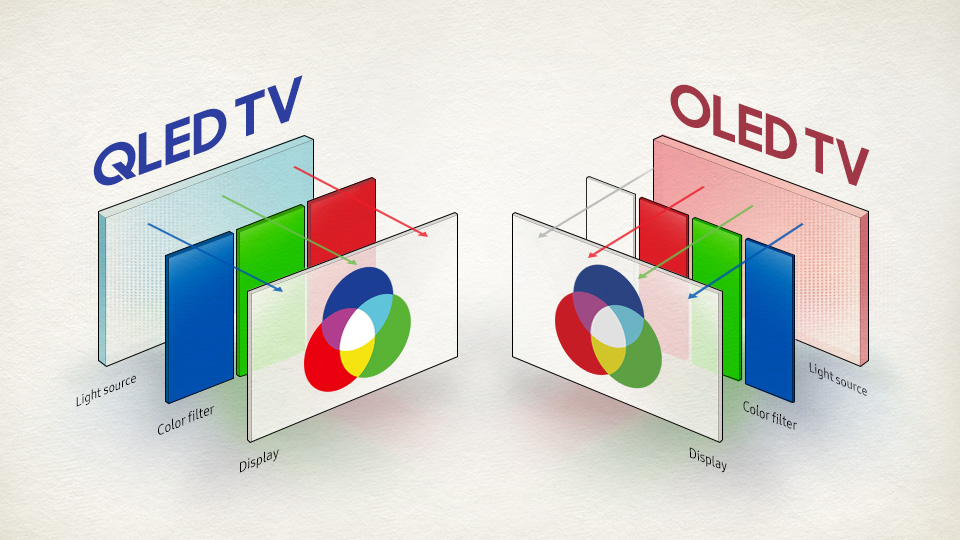

As for the large-size panel applications, OLED has gained significantly in the TV market this year as major brands such as SONY have opted for this technology in their high-end offerings. QLED, which is based on the Quantum Dot technology, has emerged as OLED’s competitor in the premium TV segment. However, QLED TVs so far has performed below expectations in terms of overall sales. OLED TVs are going to be in a dominant position in the high-end segment until the second half of 2018, when the mass production of next-generation QLED panels is expected to begin. WitsView estimates that annual global shipments of whole OLED TV sets will reach 1.5 million units for 2017 and then advance to 2.4 million units for 2018.

|

|

(Image: Samsung) |

The large-size panel market has been on the seller’s side from the third quarter of 2016 through the second quarter of this year. However, supply will begin to noticeably outpace demand starting this third quarter, leading to falling quotes. This year’s glut ratio for large-size panels is estimated at 6%, and the glut ratio for 2018 is forecast at about 8.5%, up by 2.5 percentage points. The outlook of the large-size panel market for the first half of 2018 is generally negative because the conventional seasonal effects and the expansion of Gen-10.5 capacity in China will reinforce the oversupply situation. Only by the third quarter of next year will there be a possibility of a turnaround.

TrendForce will hold its IT Industry Forecast for 2018 on the 29th of this September in Room 201 of National Taiwan University Hospital (NTUH) International Convention Center, located at No. 2, Xuzhou Road, Zhongzheng District 101, Taipei City.

For more details on this event, please visit: http://seminar.trendforce.com/TRI/AnnualForecast2017/TW/english/ or contact us via telephone or email.