Ad hoc Announcement pursuant to Art. 53 Listing Rules of SIX Swiss Exchange

ams OSRAM sharpens portfolio towards profitability and structural growth; announces profitability for Q2 at the upper end of guidance

-

Future portfolio will be focused on differentiated, intelligent sensors and emitters, with an increased commitment towards structurally attractive Automotive, Industrial and Medical markets

-

Company continues to pursue differentiated opportunities in Consumer markets, such as microLED

-

Group will exit non-core semiconductor businesses with revenue run-rate of EUR 300 to 400 million

-

Will take non-cash impairment charges on goodwill of EUR 1.3 billion

-

“Re-establish the Base” efficiency program including organizational adjustments, yielding EUR 150 million adj. EBIT run-rate improvements by end of 2025

-

Management Board will be reduced to CEO and CFO effective January 1st, 2024

-

Q2 revenues of EUR 851 million and adj. EBIT margin of 5.9% at the upper end of the guided range

-

Expected Q3 revenues of EUR 840-940 million with adj. EBIT margin of 5-8%

-

Preliminary view on FY2024: revenues will decline in 2024 due to portfolio decisions; Free Cash Flow slightly positive; core business to outgrow its target markets assuming end-markets stabilize

-

Target Financial Model revised: 6%-10% revenue CAGR based on the reduced base and adj. EBIT of approximately 15% in 2026

-

Re-financing considerations are making good progress

Premstaetten, Austria, and Munich, Germany (27 July 2023) -- ams OSRAM (SIX: AMS) presents a strategic re-alignment of the group while reporting second quarter financial results in line with the company’s expectation range.

“Over the past months, we have completed a deep analysis of the company to determine the path forward. We have a very strong core, yet we need to take significant steps to improve our performance. We are sharing key decisions today.” says Aldo Kamper, CEO ams OSRAM.

The company is re-focusing its semiconductor portfolio on its profitable core in differentiated, intelligent sensor and emitter components. The non-core and lower performing portfolio with revenues of around EUR 300 to 400 million - including amongst others - passive Optical Components, will be exited.

The automotive and specialty lighting business (Lamps & Systems Segment) with its expanding market leadership position in automotive lamps will continue to contribute meaningfully to the Group’s profitability.

ams OSRAM will expand its leading positions in the relevant automotive, industrial and medical (AIM) semiconductor markets. The Group will continue to pursue specific opportunities in the consumer device semiconductor market in product segments where it can achieve sustainable differentiation through cutting-edge innovation. It will focus its internal manufacturing capability on only those platforms that enable it to sustain differentiation versus competitors.

Going forward, investments in the core business such as high-performance LEDs and lasers, mixed-signal analog ICs and sensors will be strengthened further. The Group will continue selected investments into disruptive, future growth areas, such as microLED, but pursue a more balanced resource allocation between emerging and established opportunities.

The “Re-establish the Base” program targets annual savings of EUR 150 million by the end of 2025, approximately half of which is targeted to be realized by the end of 2024. The one-time costs of the program are estimated at EUR 50 million.

As part of this program, ams OSRAM will realize the benefits from the portfolio focusing decisions in the Semiconductor segment, as well as appropriately size the company’s overhead and infrastructure to the new revenue base. Adjustments in the managerial setup of the company will be introduced to strengthen the organization’s ability to monetize its innovation power. This entails forming two Business Units (from previously three) in the Semiconductor segment – one dedicated to emitters, the other dedicated to sensor and analog mixed signal ICs, both with clear end-to-end ownership.

With the divisional entrepreneurship strengthened, the Group moves away from a functional management model in the Management Board. As a consequence, the Group’s Management Board will be reduced to CEO and CFO, effective January 1st, 2024.

In view of the current macro-economic environment, a careful look at the prospects of each business line including some low-performing consumer businesses, revealed that the outlook required a significant reset. This led to non-cash impairment charges on goodwill of EUR 1.3 billion. The outlook for our core business remains positive.

The Group expects to grow its revenues with a CAGR of 6-10% 2023 to 2026 from the reduced base which means the new semiconductor core portfolio in the Semiconductor segment in addition to the Lamps & Systems segment.

At this revenue level and upon full implementation of its “Re-establish the Base” program, ams OSRAM expects to realize an adjusted annual operating margin (adjusted EBIT) of approximately 15% by 2026 onwards.

The Group expects to return to its 10% CAPEX of revenues over the cycle in 2025 after the currently elevated CAPEX levels driven by additional investment into establishing its new and unique 8” microLED technology platform.

Besides its progressing re-financing activities, cash-in from the exit of Semiconductor non-Core businesses and the improved cash flow generation of the core portfolio will also contribute to strengthening the balance sheet.

“Our innovation power helps simplify an increasingly complex world. As we rebuild around our core business, we will benefit from structural growth trends while making the company stronger in target markets with more differentiated offerings. It’s about being a reliable partner to all our stakeholders,” explains Aldo Kamper. “Profitability and monetizing innovation is put at the center of our thinking, whilst keeping our passion for cutting-edge technology that helps make the world safer, simpler and more efficient. This is what I will stand for together with the management team.”

Q2 financial and business update

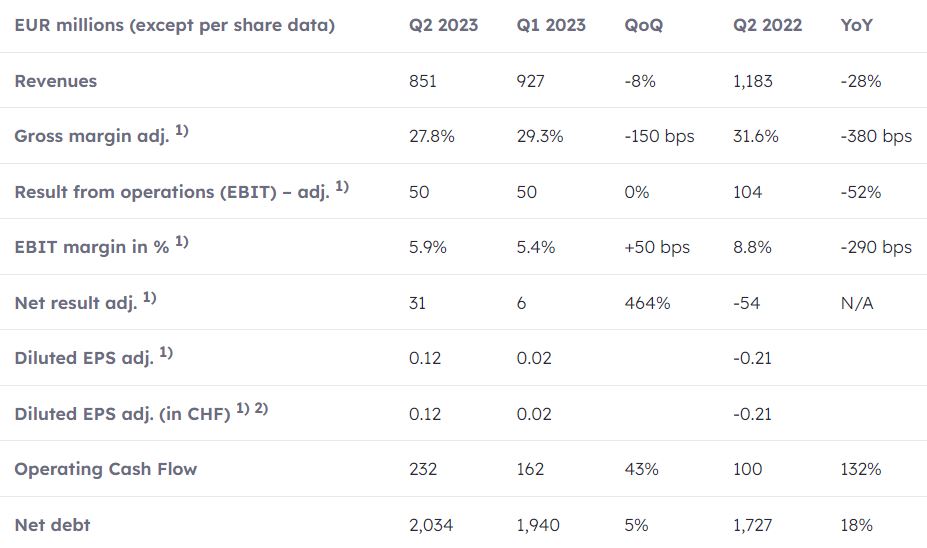

The Group reports second quarter revenues of EUR 851 million and adj. operating margin of 5.9% in line with its guidance. Excluding deconsolidation effects of EUR 79 million, which includes the sale of Digital Systems Eurasia in Q1, revenues came in essentially flat compared to the first quarter. Profitability improved slightly, coming in at the upper end of the guidance, but remained subdued especially in view of significant underutilization charges from its production and adverse product mix due to the seasonality in the L&S segment.

The Semiconductor segment, representing 71% of Q2 revenues, or EUR 600 million, showed mixed traction across the various end-markets. The automotive business showed normalizing order-patterns after almost two years of erratic behavior and inventory corrections in the wake of the various macro-economic shocks to the automotive supply chain. Industrial and Medical business performed better than in Q1, but still showed the typical mixed behavior during a macro-economic weak period with certain applications running well such as laser welding and others running very soft such as hyper-red LEDs for Horticulture lighting. The Consumer business showed signs of improvement with an 18% quarter-on-quarter increase due to higher sales from existing supply relationships. Overall, the Consumer business remains challenging for the Group compared to previous levels a year ago as the smartphone market has contracted, certain designs reach gradually End-of-Life, price pressure remains high and won designs are not yet launching until 2024.

The Lamps & Systems segment, representing 29% of Q2 revenues, or EUR 251 million, recorded robust revenues in spite of the typical seasonal decline in the Automotive aftermarket lamps business. The specialty lamps for entertainment and industrial applications sold as expected. Within that, the specialty lamps for semiconductor manufacturing equipment saw softening demand due to the global slowdown in the sector.

With the non-cash impairment of EUR 1.3 billion the IFRS net result was negative at Euro 1.3 billion. Operating Cash Flow increased significantly to EUR 232 million up by EUR 70 million compared to the first quarter.

Quarterly financial summary

-

)Excluding M&A-related, transformation and share-based compensation costs, results from investments in associates and sale of businesses

-

)Earnings per share in CHF were converted using the average currency exchange rate for the respective periods

“We were pleased to see some stabilizing trends in the Automotive LED supply chain lately. Despite better sales in certain Industrial and Consumer businesses, the macro-economic sentiment in these markets remains very challenging. We worked hard to improve our operational cash flow and will continue to work on improving our profitability”, comments Aldo Kamper.

Third Quarter Outlook

With a strengthening demand for its Automotive products, the Group expects third quarter revenues to improve to a level of EUR 840 – 940 million. The adjusted EBIT is expected to come in at 5% to 8%.

FY2024 comments

The Group will have a lower revenue base in 2024 after exiting non-Core semiconductor businesses. From this new base, including the Lamps & Systems segment, it expects revenues to outgrow its target markets, assuming end-markets stabilize.

The Group also targets slightly positive Free Cash Flow in 2024 with significantly reduced CAPEX compared to 2023, assuming end-markets stabilize.

Half-year report and additional information

Additional financial information for the second quarter as well as the half year report for the first half 2023 is available on the company website. The second quarter 2023 investor presentation incl. detailed information on the strategic update of the group is also available on the company website.

ams OSRAM will host a press call as well as a conference call for analysts and investors on the second quarter results on Friday, 28 July 2023. The press call will take place at 10.00am CEST. Journalists who would like to join the press call can register here. The conference call for analysts and investors will start at 11.00am CEST and can be joined via webcast

About ams OSRAM

The ams OSRAM Group (SIX: AMS) is a global leader in optical solutions. By adding intelligence to light and passion to innovation, we enrich people’s lives. This is what we mean by Sensing is Life.

With over 110 years of combined history, our core is defined by imagination, deep engineering expertise and the ability to provide global industrial capacity in sensor and light technologies. We create exciting innovations that enable our customers in the automotive, consumer, industrial and healthcare sectors maintain their competitive edge and drive innovation that meaningfully improves the quality of life in terms of health, safety and convenience, while reducing impact on the environment.

Our around 22,000 employees worldwide focus on innovation across sensing, illumination and visualization to make journeys safer, medical diagnosis more accurate and daily moments in communication a richer experience. Our work creates technology for breakthrough applications, which is reflected in over 15,000 patents granted and applied. Headquartered in Premstaetten/Graz (Austria) with a co-headquarters in Munich (Germany), the group achieved over EUR 4.8 billion revenues in 2022 and is listed as ams-OSRAM AG on the SIX Swiss Exchange (ISIN: AT0000A18XM4).

Gold+ Member Report

Gold+ Member Report

|

Report Title

|

Content

|

Format

|

Publication

|

|

LED Industry Demand

and Supply Database

|

Demand Market Analysis:

|

PDF / Excel

|

1Q (Mid Mar)

3Q (Early Sep)

|

|

2023-2027 Demand Market Forecast

|

|

(Backlight and Flash LED / General Lighting / Architectural Lighting / Automotive- Passenger Car & Box Truck & Scooter / Video Wall / Horticultural Lighting / UV LED / IR LED / Micro LED / Mini LED)

|

|

Supply Market Analysis:

|

|

1. LED Chip Market Value (External Sales, Total Sales)

|

|

2. WW New GaN LED and As/P LED MOCVD Chamber Installations / WW Accumulated GaN LED and As/

P LED MOCVD Chamber Installations

|

|

3. GaN LED and As/P LED Wafer Market Demand

(By Region / By Wafer Size)

|

|

4. GaN LED and As/P LED Wafer Market Demand and Supply Analysis

|

|

LED Player Revenue

and Capacity

|

LED Chip Market Analysis:

|

PDF / Excel

|

2Q (Early Jun)

4Q (Early Dec)

|

|

Top 10 LED Chip Manufacturers by Revenue and

Wafer Capacity

|

|

LED Package Market Analysis:

|

|

LED Package Manufacturers: Total Revenue, LED Revenue, and Capacity Analysis

|

|

Top 10 LED Package Providers by Revenues in Backlight and Flash LED, Lighting, Automotive, Video Wall, UV LED

|

|

LED Industry Price Survey

|

Price Survey- Sapphire / Chip / Package (Backlight, General Lighting, Agricultural Lighting, Automotive, Video Wall, UV LED, IR LED, VCSEL)

|

Excel

|

1Q (Mid Mar)

2Q (Early Jun)

3Q (Early Sep)

4Q (Early Dec)

|

|

LED Industry

Quarterly Update

|

Major Players Quarterly Update:

|

PDF

|

1Q (Mid Mar)

2Q (Early Jun)

3Q (Early Sep)

4Q (Early Dec)

|

|

EU / U.S- Lumileds, ams OSRAM, Cree LED

(Smart Global Holdings)

|

|

JP- Nichia, Citizen, Stanley, ROHM

|

|

KR- Samsung, Seoul Semiconductor, Seoul Viosys

|

|

ML- Dominant

|

|

TW- Ennostar, Everlight, LITEON, AOT, Harvatek, PlayNitride

|

|

CN- San’an, Changelight, HC SemiTek, Aucksun, Focus Lightings, Nationstar, Hongli, Refond, Jufei, MTC, MLS

|

|

Micro/Mini LED

Exhibit Report

|

CES 2023 / Touch Taiwan 2023 / Display Week 2023

|

PDF

|

Aperiodically;

<20 Pages

|

If you would like to know more details , please contact: