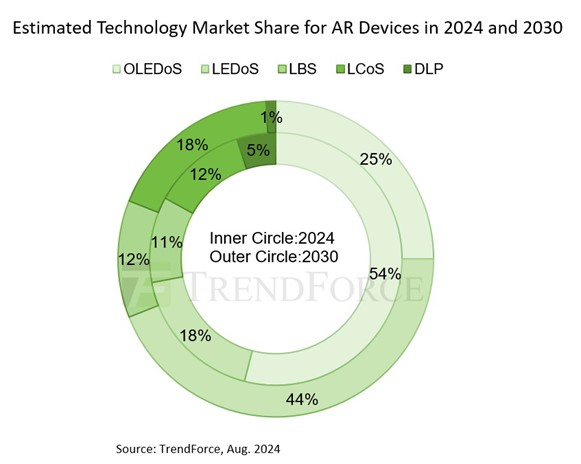

TrendForce reports that global AR device shipments are projected to reach 25.5 million units by 2030—with a CAGR of 67% from 2023 to 2030—thanks to product planning by AR brands and the advancement of AI technology and application ecosystems. Among these, the penetration of LEDoS technology is expected to rise significantly, reaching 44% by 2030, making it the mainstream technology in the market.

TrendForce notes that the popularity of AR devices is steadily increasing. In addition to brands like Apple and Meta working on AR projects, Chinese manufacturers are also investing in LEDoS. AR devices have strict requirements when it comes to the size of optical modules, how effectively high-ambient light can penetrate, and the brightness of the display system.

The display architecture of these devices includes two core systems: the optical engine, which determines refresh rate, color, and brightness limits, and the optical system, which controls imaging. Together, these systems influence key performance indicators such as PPD, FOV, and optical efficiency.

LEDoS market share to reach 44% as it surpasses OLEDoS

LEDoS is regarded as an essential technological reserve given its ability to meet certain requirements for AR devices, such as low power consumption, small size, and high brightness. In the short term, this technology is gaining support from brand manufacturers due its advantages in AR displays—as evidenced by the collaboration between Porotech and Foxconn to broaden the technology’s uses.

However, LEDoS currently faces challenges such as improving the luminous efficiency of micro-scale LEDs and achieving full-color displays in very small spaces. Nevertheless, as vertical chip stacking and color conversion technologies mature in the coming years, its penetration rate will continue to rise. TrendForce estimates that LEDoS will have an 18% market share in AR devices in 2024 and grow to 44% by 2030.

TrendForce further points out that, based on current cost structures, market conditions, and technological maturity, OLEDoS is currently the only technology that can be used in both VR/MR and AR devices. OLEDoS, combined with BirdBath optics, is presently the most cost-effective and display-efficient solution. Although OLEDoS resolution is rapidly improving, it still struggles with balancing brightness and color display in AR applications. With its market share expected to be impacted by the rise of LEDoS, OLEDoS’s share in AR devices is projected to decline from 54% in 2024 to 25% by 2030.

Brand investments help LCoS maintain market position

Compared to LEDoS or OLEDoS, LCoS boasts high resolution and brightness, with advantages in production yield and cost. However, the design of the polarization beam-splitting prism in LCoS limits further miniaturization of optical modules, posing a long-term threat of being replaced in the high-end market by the maturing LEDoS. Yet, despite this issue, with continued technological development investments from brands like Meta, LCoS is expected to maintain a certain market share in AR devices. TrendForce forecasts LCoS will have a 12% market share in 2024, growing to approximately 18% by 2030.

TrendForce also mentions that LBS technology, which uses laser light sources with fast response times, is limited by refresh rate and resolution due to its use of rapid raster scanning to continuously display images. Its market share is expected to remain stable at around 10% to 12% from 2024 to 2030. Meanwhile, DLP faces significant challenges in meeting the high-resolution requirements of AR and lacks sufficient support from brand manufacturers, with its market share in AR devices projected to shrink to 1% by 2030.

TrendForce 2024 Near-Eye Display Market Trend and Technology Analysis

Release Date:2024 / 07 / 31

Languages:Traditional Chinese / English

Format:PDF

Page:164

|

If you would like to know more details , please contact:

|