The U.S. Department of Energy (DOE) recently published its latest Solid State Lighting (SSL) Manufacturing R&D Roadmap for 2013. The Roadmap complements the SSL R&D Multi-Year Program Plan that guides the Core and Product Development R&D programs. According to DOE press release, the roadmap is an extension of the 2012 roadmap.

Some of the key findings in the latest report include:

-

LED manufacturing has benefited greatly from the rapid growth in LED-backlit displays. As a result, there is less of a need for attention on the basic LED chip manufacturing equipment and process. The most important needs are more specific to lighting. SSL Manufacturing Roadmap.

-

Luminaire manufacturing is changing dramatically in response to the new technology, with less emphasis on the lamp-fixture paradigm and increasing emphasis on integrated luminaires to minimize cost and maximize efficacy.

-

Highly flexible luminaire and module manufacturing will be needed to address the rapidly expanding market. That is, to be able to accommodate the enormous variety of designs demanded by customers for multiple applications, lines will need to be efficient and cost-effective even with relatively low numbers for any given code. This may call for innovative methods and equipment.

-

While there is potential for color-mixed solutions, much basic work remains to make that practical. The workhorse for current lighting products is phosphor-converted blue light, and there is still potential for energy improvement and cost reduction in that technology.

-

The overriding barrier to adoption of OLED lighting is the high cost of OLED panels. Until that can be overcome, manufacturing efforts on OLED luminaires, while needed, may not be the highest priority.

-

Although there is controversy about the appropriate scale, OLED deposition equipment is one place where some impact may be made. In particular there is a need for high yield processes and innovative approaches.

-

Improvements in the materials supply for OLED manufacture represent an opportunity for cost reductions and increased performance, particularly in regards to integrated substrates and encapsulation.

The report noted the biggest challenge for the LED industry at the moment is to expand and accommodate demand, while the OLED industry needs to cut down costs to provide affordable products.

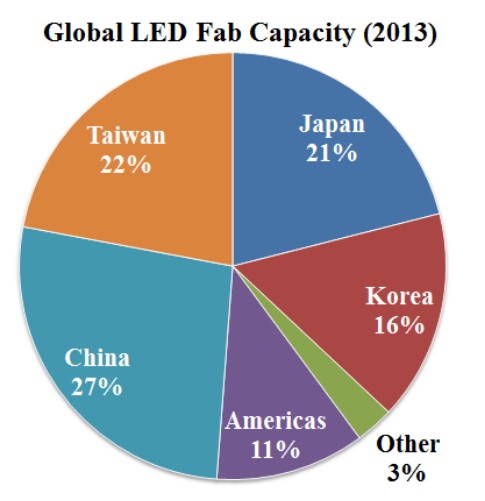

Analysis of global manufacturing by the DOE show Chinese manufacturers are now the largest group in LED manufacturing taking 27% market share followed by Taiwanese manufacturers 22% and Japan’s 21%.

|

|

Global LED manufacturing distribution in the DOE latest SSL report. (LEDinside/ DOE) |