Ad hoc Announcement pursuant to Art. 53 Listing Rules of SIX Swiss Exchange

-------------------------------------------------------

ams OSRAM delivers solid EUR 881m Q3 revenues, 19% adj. EBITDA and upsizes strategic savings program by another EUR 75m run-rate savings

-

Q3/24: revenues EUR 881m (at the midpoint of the guided range), adj. EBITDA EUR 166m (18.8%,

above the midpoint of the guided range), adj. EBIT EUR 82m (9.3%), supported by NREs

-

Q3/24: free cash flow (incl. net interest) EUR 188m, significantly improved by good operational

performance, lower CAPEX and supported by customer prepayment & NREs (together approx. EUR

250m)

-

Q3/24: strong cash position of EUR 1.1bn

-

Design-win momentum continues with deepening customer relationships, standing at EUR 3.5bn (lifetime-value) year-to-date

-

Execution of “Re-establish the Base” program progressing well, approx. EUR 85m run-rate savings

realized to date, ahead of schedule

-

Upsizing “Re-establish the Base” program by another EUR 75m run-rate savings to reach in total

approx. EUR 225m by end of 2026 to safeguard profitability improvements in an uncertain

environment; more than 500 non-production employees will be affected, additionally

-

Mid-term Target Operating Model updated for 2024-2027: core-semiconductor business to grow

6% to 10% and adj. EBITDA margin for the group to reach 20% to 24% by 2027 at 8% CAPEX to

Sales

-

Q4/24: expected fourth quarter revenues of EUR 810m to 910m and adj. EBITDA margin of 15% to

18% in line with seasonality of business mix

-

Comment on Q1/25: company expects a weak Q1, but sees growth in its semiconductor coreportfolio

for the full year

Premstaetten, Austria, and Munich, Germany (07 November 2024) -- ams OSRAM delivers solid

EUR 881m Q3 revenues, 19% adj. EBITDA margin supported by NRE, pos. FCF of EUR 188m and

upsizes strategic efficiency program “Re-establish the Base” by EUR 75m run-rate savings

“We are progressing faster with implementing our strategic efficiency program ‘Re-establish the Base’ as

planned. Given that cyclical weakness in key markets persists, further cost savings are required to

sustain our trajectory towards industry benchmarks while continuing our investment to exploit structural

growth paths in our semiconductor target markets. Therefore, we are stepping up our ‘Re-establish the

Base’ program by another 75 million Euro run-rate savings – to be realized by the end of 2026,” said Aldo

Kamper, CEO of ams OSRAM.

Q3/24 financial update

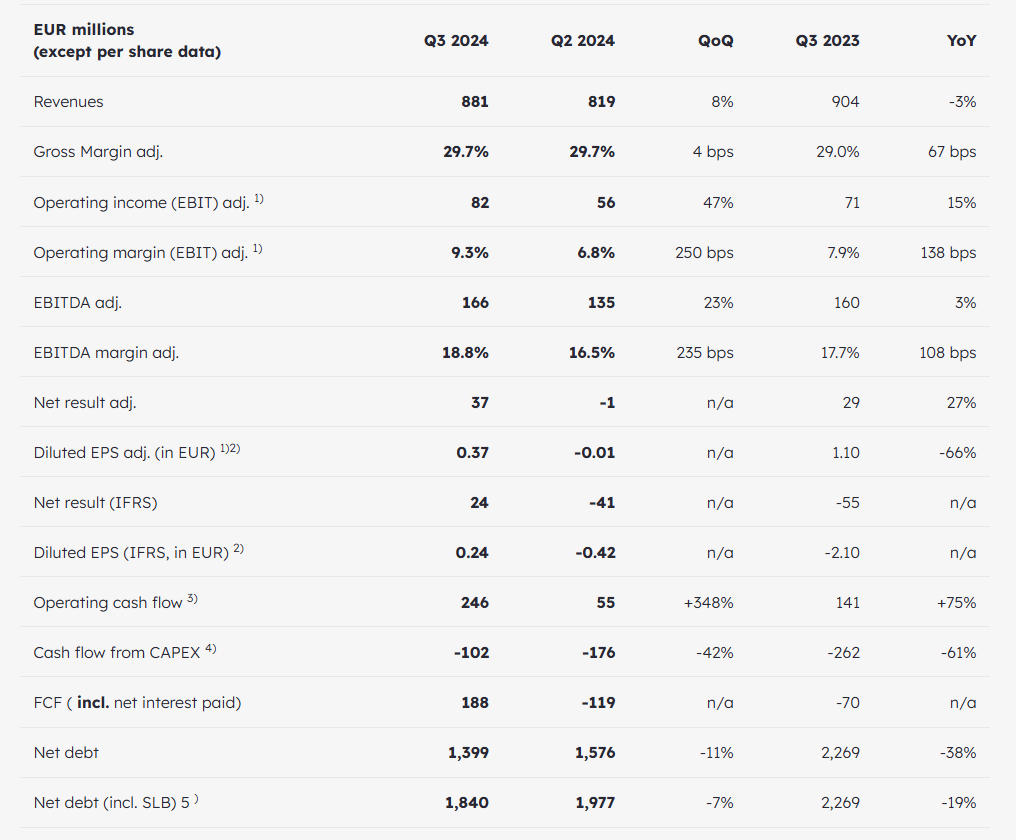

ams OSRAM announces revenues of EUR 881 million for the third quarter 2024, at the midpoint of the

guided range of EUR 830 – 930 million. Revenues increased 8% quarter-over-quarter, primarily driven by the ramp of new semiconductor products for consumer handheld applications, the seasonal high of LED products for horticulture and NREs (including catch-up) for development of novel LED technologies,

whilst the product mix showed seasonal and cyclical shifts overall.

Year-over-year, the group records a slight revenue decline of 3% which is entirely attributable to the

segment Lamps & Systems. The semiconductor business came in flat year-over-year with EUR 647

million revenues in Q3, compared to EUR 648 million a year ago. Excluding the non-core portfolio, a midsingle-digit growth in the relevant core portfolio is visible year-over-year.

The adjusted EBITDA (adjusted earnings before interest, taxes, depreciation, and amortization, i.e.

operating margin adjusted for special, non-operational effects) came in at EUR 166 million, i.e. at 18.8%

adj. EBITDA margin, above the midpoint of the guided range of 17% - 20%, supported by one-offs such

as NREs. Further details are described further down in the commentary on the segments.

The adjusted EBIT (adjusted earnings before interest and taxes, i.e. operating margin adjusted for

special, non-operational effects) margin for the group came in at 9.3%. In absolute terms, the adjusted

EBIT amounted to EUR 82 million.

“Re-establish the Base” program implementation status & upsizing

Implementation of current program

On 27 July 2023, the company announced its strategic efficiency program “Re-establish the Base”, which

was aimed at focusing the company on its profitable, structurally growing core. It targets EUR 75 million

run-rate savings by end of FY2024 and EUR 150 million run-rate savings by end of FY2025 compared to

2023 actuals.

To date, the company has realized already EUR 85 million savings, reaching the EUR 75 million run-rate

savings mark earlier than anticipated. Recent implementation successes are especially evident when

looking at the profitability improvement of the CSA segment.

At the start of the program in 2023, the company’s non-core semiconductor portfolio represented approx.

EUR 300 – 400 million. In FY2024, close to EUR 200 million of those are still part of the group revenues.

The company is exiting this remaining, loss-making, non-core business through product end-of-life, which

will be largely completed by the end of 2024, after it had sold the passive optical components assets and

restructured its CMOS image sensors business earlier this year. Several sizeable new design-wins in

consumer device applications are expected to compensate for the revenue loss from those product

discontinuations.

Upsizing “Re-establish the Base”

In view of the persisting market uncertainties in 2025, especially when it comes to the automotive sector,

the company has decided to up-size and extend its strategic efficiency program by around EUR 75

million run-rate savings to be effective by the end of 2026. The extended program addresses especially

company footprint considerations to get step-by-step even closer to industry benchmarks with regard to

overhead, corporate and manufacturing footprint. The program extension will affect additionally more

than 500 non-production employees. Out of this number, approx. one third of functions are planned to be

relocated to best-cost countries. In total, the program is expected to deliver EUR 225 million run-rate

savings by the end of 2026. The company expects approx. EUR 40 million of additional transformation

cost due mostly in 2025.

Advancing the mid-term Target Operating Model to 2024-2027

With largely completing the exit of the non-core semiconductor portfolio by end of 2024, the company

sharpens its focus on structural growth in its semiconductor core markets. Based on this year’s

semiconductor core revenues (which are defined excluding approx. EUR 200 million of non-core

business which is being exited as described above), the company intends to grow its semiconductor

business with a CAGR between 6% and 10% until end of 2027. The traditional lamps business is

expected to develop in a corridor of flat or slightly down.

Previously, the company was assuming for the core-semiconductor portfolio together with the L&S a

CAGR of 6% to 8% for the period 2023-2026.

With its focus on improving cash generation, the company also switches its profitability benchmark to

EBITDA. The levers of its profitability improvement remain unchanged. Firstly, structural cost-savings

and efficiency improvements from its “Re-establish the Base” program. Secondly, ramp of new products

and design-wins. Thirdly, market recovery in target markets. As the market recovery in important markets

(such as industrial) is delayed and additional and temporary weakness in some core markets like

automotive is seen, the company now expects to reach an adjusted EBITDA of 20% to 24% by 2027.

The revised CAPEX to Sales target ratio is 8%.

Previously, the company assumed reaching an adjusted EBIT of approx. 15% by 2026 at a CAPEX to

Sales target ratio of 10%.

Semiconductor business update

Opto Semiconductors segment (OS)

Revenues for opto-electronic semiconductors increased by EUR 9 million to EUR 381 million in Q3/24

compared to EUR 372 million in Q2/24. Adjusted EBITDA stood at EUR 88 million, representing an

adjusted EBITDA margin of 23%.

NRE payments for the development of LED technologies were essential for the quarter-over-quarter

revenue and adj. EBITDA improvement and exemplify the company’s leading technology position. As

expected, Automotive revenue contribution was down quarter-over-quarter. A catch-up of government

subsidies also contributed to the strong adj. EBITDA of the OS segment.

CMOS sensors and ASICs segment (CSA)

Revenues for CMOS sensors and ASICs increased to EUR 266 million in Q3/24, up from EUR 224

million in Q2/24. The 19% quarter-over-quarter increase was mainly driven by the ramp of a new sensor

product for consumer device applications.

Adjusted EBITDA more than doubled to EUR 48 million in Q3/24, up from EUR 21 million in Q2/24,

representing an adjusted EBITDA Margin of 17.9%. In Q2/24, the adj. EBITDA margin stood at 9.4%.

The two-fold increase is driven by significantly higher sales, therefore much lower underutilization cost,

additional gross profit and savings from implementing the Re-establish-the-Base program.

The industrial and medical businesses are still suffering from persistent inventory corrections in the

supply chain.

Semiconductors industry dynamics

Revenues from the two semiconductor business units represented 73% of Q3/24 revenues, or

correspondingly EUR 647 million. This compares to EUR 648 million a year ago, essentially flat. Endmarkets continued to show different cyclicality. Revenues from consumer applications compensated for cyclically weaker revenues in automotive, industrial, and medical applications. Excluding the non-core

portfolio (in FY23 around EUR 350 million, for FY24 around EUR 200 million estimated), the company

sees a mid-single-digit percentage growth in the core portfolio year-over-year.

Automotive:

The automotive business performed reasonably well in a weakening market environment, which was

illustrated by a string of profit warnings from car OEMs. The year-over-year decline of 9% and quarterover-quarter decline of 7% is in line with the overall situation in the automotive market.

Industrial & Medical (I&M):

The business showed a mixed performance and landed essentially flat quarter-over-quarter, exhibiting an

8% decline compared to a year ago. The persisting inventory corrections for medical technology and

industrial capital goods businesses are still weighing heavily on the groups I&M semiconductor business.

The sale of LED emitters into professional lighting applications was relatively healthy, whilst product

sales into horticulture applications showed its seasonal peak.

Consumer:

With the ramp of new products and healthy overall sales of consumer hand-held devices and wearables,

the business showed a significant increase of 24% year-over-year. Quarter-over-quarter, the increase

was even higher, standing at 45%.

New business wins – Design-wins:

The company managed to intensify and deepen its relationship with various key customers during the

quarter, which resulted not only in the previously mentioned NRE funded technology development

projects and a prepayment for the development & production of new products, but also in unabated

design-win momentum, across all product categories of the core semiconductor portfolio. Several

meaningful consumer design-wins are standing out. The company added EUR 1 billion of new future

business during the third quarter, totaling EUR 3.5 billion year-to-date, measured in estimated life-timevalue of each individual design won.

Lamps & Systems segment (L&S)

The Lamps & Systems segment represented 27% of Q3/24 revenues, equaling EUR 233 million. A 5%

quarter-over-quarter increase. The year-over-year reduction comes mainly from discontinued OEM

products and a slight decline in the traditional business.

Adjusted EBITDA in Q3 came in at EUR 37 million or 16% adjusted EBITDA margin.

Automotive:

The automotive aftermarket business was still off-season during the summer months. The OEM business

was as expected, including planned end-of-life of legacy module businesses amongst other dynamics.

The company typically sees its strongest demand in Q4 and Q1 of a year when high halogen bulb

replacement rates can be seen in the European and North American aftermarket.

Specialty Lamps:

Industrial and professional entertainment markets are still impacted by persistent inventory correction

and weakness whilst revenues remained on a comparable level as in previous quarters.

Additional key financial figures

Gross margin

The adjusted gross margin remained flat quarter-over-quarter and increased 70 basis points year-over-year due to improved factory loading and contributions from the “Re-establish the Base” program.

Net result & earnings per share

The adjusted net result came in at 37 EUR million in Q3/24 from EUR 29 million a year ago and up from

EUR -1 million in the second quarter. Various one-off effects, such as NRE, funding catch-up and

reduced re-structuring cost were key to this development.

On 30 Sep 2024, a reverse split in a ratio of 10:1 was executed. The figures for earnings per share of

previous quarters have been backward adjusted for comparison purposes.

Consequently, third quarter adjusted basic earnings per share came in at 0.37 EUR, significantly up

compared to the EUR -0.01 EUR in the second quarter.

Third quarter adjusted diluted earnings per share came in at 0.37 EUR, also significantly higher than the

EUR -0.01 in the second quarter.

The IFRS net result stood at EUR 24 million in Q3/24 after EUR -41 million in the second quarter. As

mentioned above, one-off effects supported that significant improvement. Consequently, the basic IFRS

earnings per share came in at EUR 0.24 in Q3/24, after EUR -0.41 in Q2/24. The diluted IFRS earnings

per share amounted to EUR 0.24 in Q3/24 after EUR -0.42 in Q2/24.

Cash flow

Customer pre-payments & NREs

In Q3/24, ams OSRAM received both a prepayment for the development & production (i.e. securing

supply-chain availability) of new products and NREs for the development of LED technologies from

various customers. The received amounts total approx. EUR 250 million, exemplifying the leading

technology position of the company in its target markets.

The prepayment is a non-financial liability that will be repaid through the delivery of products starting in

2026.

The NREs are payments for the development of certain novel LED technologies that may or may not lead

to future products and are not refundable or re-payable.

Operating cash flow (including net interest paid) came in at EUR 246 million in Q3/24, significantly

improved by the aforementioned customer prepayment (approx. EUR 225 million).

Cash flow from investments into PPE and intangibles, or CAPEX, came down significantly to EUR -102

million compared to EUR -176 million in the previous quarter. Cash flow from CAPEX was substantially

lower than a year ago (EUR -262 million), as CAPEX spendings are approaching the target CAPEX to

Sales ratio. Some CAPEX overhang persists from the cancelled microLED cornerstone project in

conjunction with equipment that could not be cancelled anymore.

Free cash flow – defined as operating cash flow including net interest paid minus cash flow from CAPEX

plus proceeds from divestments – came in strong at a positive EUR 188 million in Q3/24 after EUR -119

million in Q2/24.

Net-debt related financial figures

The gross cash position increased to EUR 1,097 million in Q3/24 after EUR 900 million in Q2/24. Main

elements contributing to the increased cash balance were the operational performance with improved

EBITDA, the customer prepayment, the extension of the EUR denominated senior notes by EUR 200

million (nominal), offset by the re-payment of a short-term bi-lateral facility and a promissory note

(together ~EUR 150 million), as well as reducing supply chain financing.

Consequently, the net debt position decreased to EUR 1.399 million quarter-over-quarter after EUR

1,576 million in Q2/24.

When including EUR 441 million equivalent from the Sale-and-Lease Back Malaysia transaction (booked

under other financial liabilities), the net debt position decreased accordingly to EUR 1,840 million in

Q3/24 compared to EUR 1,977 in Q2/24.

Update of transformation costs

The company excludes transformation costs from its operational performance measures, i.e. adj.

EBITDA and adj. EBIT. Transformation costs in 2024 are mainly driven by the adjustment of its microLED

strategy and its “Re-establish the Base” program.

Adjusting the microLED strategy led to impairment charges of EUR 513 million and transformation costs

of EUR 108 million in H1/24, including non-cash accruals. In Q3/24, the company recorded a net gain of

approx. EUR 20 million as a consequence of the reversal of some provisions. In summary, the company

now expects in total up to EUR 660 million of transformation cost related to adjusting the microLED

strategy including impairments (from previously EUR 680 million).

Transformation costs related to “Re-establish the Base” were approx. EUR 8 million in Q3/24. For FY

2024, the company now expects up to EUR 40 million which could include an additional approx. EUR 15

million from upsizing the program compared to the expectation end of Q2.

Moreover, additional details on the bridge from EBITDA according to IFRS to adj. EBITDA can be found

in the investor presentation on the company’s website.

Status of outstanding OSRAM minority shares

On 30 September 2024, the Group held around 86% of OSRAM Licht AG shares. The total liability for

minority shareholders’ put options stood almost unchanged at EUR 604 million at the end of Q3/24

compared to EUR 605 million at the end of Q2/24.

The company has a Revolving Credit Facility (RCF) in place. The RCF is primarily in place to cover any

further significant exercises under the 'domination and profit and loss transfer agreement (DPLTA)’ put

option and would be sufficient to fully cover all outstanding minority shareholders’ put options. It could

also be drawn for general corporate and working capital purposes.

Fourth quarter 2024 Outlook

The company sees flattish demand for its automotive semiconductor products in Q4/24 reflecting the

uncertainties in the global automotive supply chain. The demand from industrial and medical markets

remains very muted in some segments. The business with its semiconductor products for consumer

handheld devices and horticulture will see a seasonal slowdown in the fourth quarter.

Looking at the L&S segment, the automotive aftermarket halogen lamps business will see a seasonal

demand upswing when entering the short daylight season in the Northern hemisphere.

As a result, the group expects fourth quarter revenues to go down a bit due to seasonal mix effects and

land in a range of EUR 810 – 910 million. Consequently, the adj. EBITDA is expected to come in

between 15% – 18% driven by revenue fall-through and some cost headwinds. The EUR/USD exchange

rate is assumed to be 1.10.

Comments on FY 2024

The company continues to expect CAPEX for FY2024 to come in between EUR 500 – 550 million

(including capitalized R&D and rolled-over accounts payable related to PPE from 2023).

The company continues to target a positive free cash flow before net interest paid for the full year 2024.

Comments on FY 2025

The company expects a weak start into 2025 with weaker revenues in the first Quarter of 2025 than one

would expect from seasonal mix effects. In particular, the company expects the cyclical weakness in its automotive business to become fully visible in the first quarter, with gradual, steady improvement during

the FY. Consequently, the company still expects growth in its semiconductor core-portfolio in 2025.

The company will also target a positive free cash flow including net interest paid for the full year 2025.

Additional Information

Additional financial information for the third quarter 2024 is available on the company website. The third

quarter 2024 investor presentation incl. detailed information is also available on the company website.

ams OSRAM will host a press call as well as a conference call for analysts and investors on the third

quarter results on Thursday, 07 November 2024. The conference call for analysts and investors will start

at 10.00 am CET and can be joined via webcast. The conference call for journalists will take place at

11.00 am CET.

Key financial figures

-

Adjusted for M&A-related, transformation and share-based compensation costs, results from investments in associates and sale of businesses.

-

Earnings per share are not comparable between the years due to the capital increase on 7 December 2023 whereby additional 724,154,662 shares were issued. Comparative figures were adjusted following the 10:1 reverse share split on 30 September 2024.

-

From Q1 2024, operating CF includes net interest paid; 2023 figures reclassified for comparison.

-

Cash flow from investments in property, plant, and equipment and intangibles (such as capitalized R&D).

-

Incl. EUR 441m equivalent as of end of September 2024 from SLB Malaysia transaction closed in December 2023.

About ams OSRAM

The ams OSRAM Group (SIX: AMS) is a global leader in intelligent sensors and emitters. By adding intelligence to light and passion to innovation, we enrich people’s lives.

With over 110 years of combined history, our core is defined by imagination, deep engineering expertise and the ability to provide global industrial capacity in sensor and light technologies. We create exciting innovations that enable our customers in the automotive, industrial, medical and consumer markets to maintain their competitive edge and drive innovation that meaningfully improves the quality of life in terms of health, safety and convenience, while reducing impact on the environment.

Our around 20,000 employees worldwide focus on innovation across sensing, illumination and visualization to make journeys safer, medical diagnosis more accurate and daily moments in communication a richer experience. Our work creates technology for breakthrough applications, which is reflected in over 15,000 patents granted and applied. Headquartered in Premstaetten/Graz (Austria) with a co-headquarters in Munich (Germany), the group achieved EUR 3.6 billion revenues in 2023 and is listed as ams-OSRAM AG on the SIX Swiss Exchange (ISIN: AT0000A3EPA4).

Find out more about us on https://ams-osram.com

ams is a registered trademark of ams-OSRAM AG. In addition, many of our products and services are registered or filed trademarks of ams OSRAM Group. All other company or product names mentioned herein may be trademarks or registered trademarks of their respective owners.

Gold+ Member Report

Gold+ Member Report

|

Report Title

|

Content

|

Format

|

Publication

|

|

LED Industry Demand

and Supply Database

|

Demand Market Analysis:

|

PDF / Excel

|

1Q (Mid Mar.)

3Q (Early Sep.)

|

|

2024-2028 Demand Market Forecast

|

|

(Backlight and Flash LED / General Lighting / Agricultural Lighting / Architectural Lighting / Automotive- Passenger Car & Box Truck & Scooter / Video Wall / UV LED / IR LED / Micro LED / Mini LED)

|

|

Supply Market Analysis:

|

|

1. LED Chip Market Value (External Sales, Total Sales)

|

|

2. WW New / Accumulated GaN LED and AS/P LED MOCVD Chamber Installations

|

|

3. GaN LED and AS/P LED Wafer Market Demand (By Region / By Wafer Size)

|

|

4. GaN LED and AS/P LED Wafer Market Demand and Supply Analysis

|

|

LED Player Revenue

and Capacity

|

LED Chip Market Analysis:

|

PDF / Excel

|

2Q (Early Jun.)

4Q (Early Dec.)

|

|

Top 10 LED Chip Manufacturers by Revenue and Wafer Capacity

|

|

LED Package Market Analysis:

|

|

LED Package Manufacturers: Total Revenue, LED Revenue, and Capacity Analysis

|

|

Top 10 LED Package Players by Revenues in Backlight and Flash LED, Lighting, Automotive, Video Wall, UV LED

|

|

LED Industry Price Survey

|

Sapphire / Chip / Package (Backlight, General Lighting, Agricultural Lighting, Automotive, Video Wall, UV LED,

IR LED, VCSEL)

|

Excel

|

1Q (Mid Mar.)

2Q (Early Jun.)

3Q (Early Sep.)

4Q (Early Dec.)

|

|

LED Industry

Quarterly Update

|

Major Players Quarterly Update:

|

PDF

|

1Q (Mid Mar)

2Q (Early Jun)

3Q (Early Sep)

4Q (Early Dec)

|

|

EU / U.S.- Lumileds, ams OSRAM, Cree LED

(Smart Global Holdings)

|

|

JP- Nichia, Citizen, Stanley, ROHM

|

|

KR- Samsung, Seoul Semiconductor, Seoul Viosys

|

|

ML- Dominant

|

|

TW- Ennostar, Everlight, LITEON, AOT, Harvatek, PlayNitride

|

|

CN- San’an, Changelight, HC SemiTek, Aucksun, Focus Lightings, Nationstar, Hongli, Refond, Jufei, MTC, MLS

|

|

Micro/Mini LED

Exhibit Report

|

CES 2024 / Touch Taiwan 2024 / Display Week 2024

|

PDF

|

Aperiodically;

<20 Pages

|