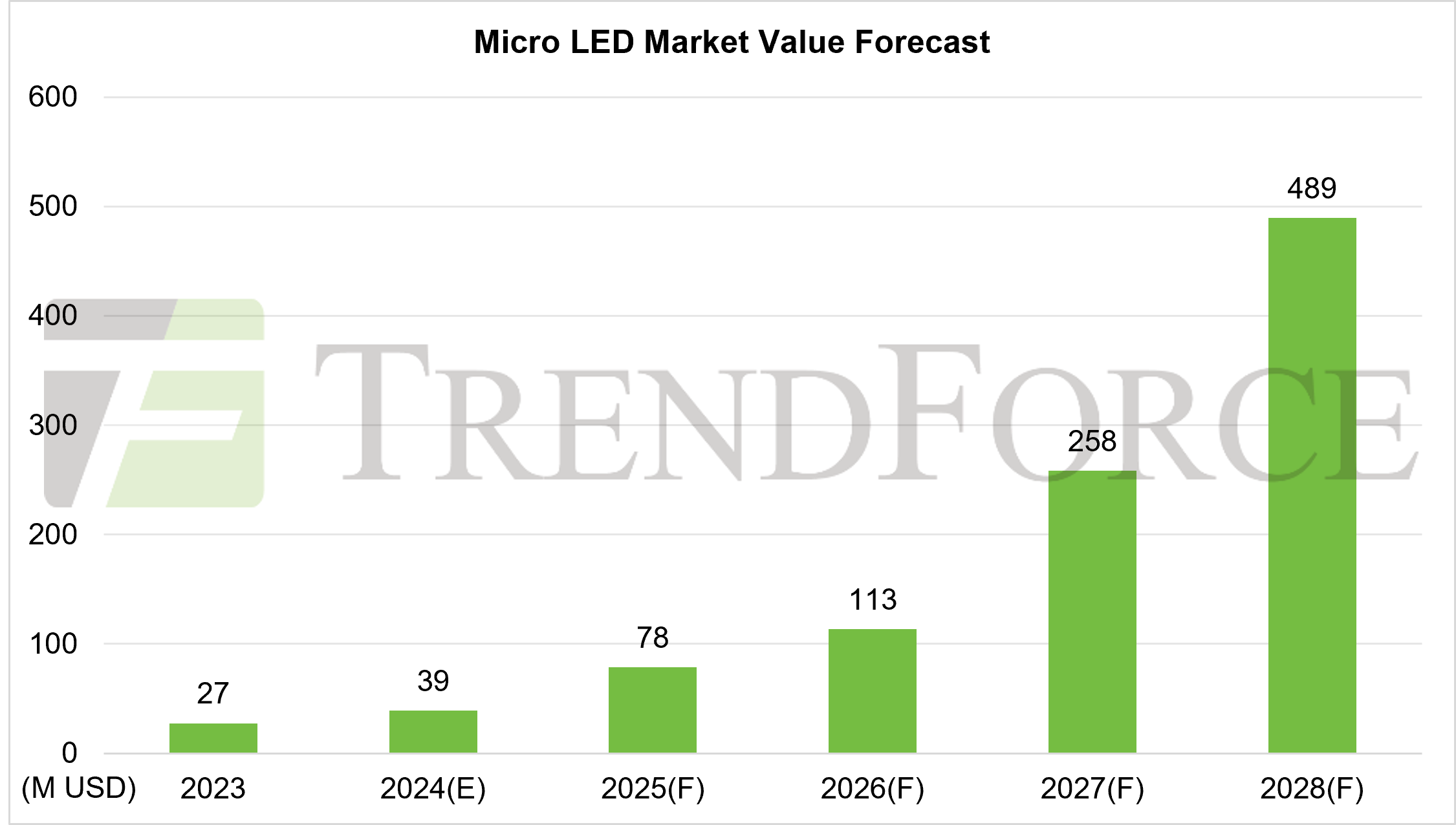

TrendForce reports that the revenue from Micro LED chips is projected to reach approximately US$39 million in 2024, with large displays remaining the primary source of contribution. Looking ahead, breakthroughs in technical bottlenecks are on the horizon, while applications in automotive displays and the increasing maturity of full-color AR glasses solutions are expected to propel Micro LED chip revenue to $489 million by 2028.

TrendForce highlights several challenges confronting the Micro LED industry in 2024. First, the slow progress in chip miniaturization has hindered cost-reduction efforts. Second, the high price of Micro LED displays has resulted in weak end-user demand, limiting the shipment scale of large-sized displays already in production. Third, the focus in the wearable device market has shifted to software optimization and hardware-software integration. This has reduced the incentive for brands to innovate hardware and slowed the adoption of new display technologies like Micro LED. Lastly, while automotive applications remain a key area of promise for Micro LED, they are still in the early stages of adoption and validation, making it difficult to contribute significantly to revenue in the short term.

From a technical perspective, addressing the challenge of seamless large-sized display assembly is crucial. In the short term, improving backplane production yield through different driving schemes can enhance efficiency and reduce costs. Over the medium to long term, increasing backplane size to minimize the number of required assemblies could eliminate complex manufacturing steps such as side wiring and TGV(Through Glass Via).

Additionally, maximizing light extraction efficiency is becoming increasingly important in Micro LED display design and production. Techniques such as microstructure and reflective structure design can reduce light loss and improve brightness by optimizing reflected light.

TrendForce points out that as the yield rate of mass transfer technology improves, new challenges are emerging in inspection processes. Although the LED industry already has established testing methods, these solutions require refinement to handle the extreme miniaturization and high volume of Micro LED chips. Addressing these inspection challenges is currently a critical priority for the industry.

Micro LED’s standout characteristics—high brightness, high contrast, and high transparency—continue to attract investment from manufacturers. These features enable Micro LED to integrate into transparent displays for automotive windows or as part of AR-HUD or P-HUD systems, meeting the growing demand for seamless integration of virtual and real-world information for drivers and passengers. Additionally, combining Micro LED with silicon substrates offers a robust solution for near-eye displays in AR glasses, positioning Micro LED as a benchmark for next-generation metaverse-focused head-mounted devices.

TrendForce emphasizes that the commercialization of Micro LED technology should not overly depend on the mature consumer electronics market. Instead, manufacturers should capitalize on Micro LED’s unique display capabilities, pairing them with diverse sensor solutions to empower devices with new functionalities and uncover imaginative niche applications. This strategy is expected to accelerate Micro LED's penetration across various markets, further driving growth and innovation.

Author: Thea, Eric

TrendForce 2024 Micro LED Market Trend and Technology Cost Analysis

Release: 31 May / 30 November 2024

Language: Traditional Chinese / English

Format: PDF

Page: 160-180

Chapter I. Micro LED Toatl Market Analysis

-

2024-2028 Micro LED Market Size Analysis

-

2024-2028 Micro LED Wafer Demand Analysis

Chapter II. Micro LED Substrate Material and Technology Analysis

-

Micro LED Technology Portfolio Roadmap

-

Micro LED Diversified Substrate Options

-

GaN-on-GaN Micro LED Solve the Wavelength Shift Problem

-

Micro LED on Ge Opens Up to a New Opportunity

-

Wafer Material Selection Strategies

-

Intrinsic Differences between Micro LED and OLED Light Sources

-

Micro LED Optical Challenges

-

Micro LED Optical Structures for LEE Optimization

-

Intrinsic Limitations of LED Light Sources: Light Concentration Challenge

-

On-chip Optics: Micro-optics is a New Focus

-

Fluid Transfer Technology featuring Dynamic LED Alignment

-

Fluid Transfer System Strategically Shifts to COC

-

Considerations in Different Transfer Stages

-

Chip Structure Selection from Manufacturing Integration Perspective

-

Micro LED 2024 Technology Development Highlights

Chapter III. Micro LED Large-Sized Displays

-

2024-2028 Micro LED Market Size Analysis : Large-sized Display

-

2024-2028 Micro LED Market Size Comparison : Large-sized Display

-

Four Stages from Splicing to Single Panel

-

Combination of Light Source with Driver Circuit

-

Driver on Micro LED Technology Overview

-

Evolving Monolithic Integration Technology: IGZO on Micro LED

-

Different Driving Modes: PAM, PWM, PHM

-

PAM to Be Mainstream in Low-grayscale Driving

-

Simultaneous and Progressive Emission Driving Modes

-

Progressive Emission increases the Chance of PWM for Micro LED

-

Self-emitting Displays Driving Modes Lead to the Same Outcome

Chapter IV. Micro LED Small and Medium Displays

4.1 Wearable Devices

-

2024-2028 Micro LED Market Size Analysis: Wearable Devices

-

Micro LED–Sensor Integration Challenges

4.2 Head-mounted Devices

-

2024-2028 Micro LED Market Size Analysis: Head-mounted Devices

-

2024-2028 Micro LED Market Size Comparison: Head-mounted Devices

-

Wire / Rod Micro LED: An Edge in Efficiency for High PPI Applications

-

Micro LED Technology Evaluation for NED

-

Material Options for AR Glasses Waveguides

-

Orion Double-sided Grating Waveguide

-

Fresnel and Pancake Lenses Co-exist to Achieve Market Segmentation

4.3 Automotive Display

-

2024-2028 Micro LED Market Size Analysis: Automotive Displays

-

Micro LED Challenge: Addressing Color Shift at High Temperatures

-

Automotive Display Issues Vary Greatly Between Day and Night

-

High Brightness Needed on Concrete Roads to Meet Contrast

-

Chapter V. Micro LED Commercial Development Analysis P86

-

Micro LED R&D Focus Shifts from Front to Back Process

-

AI as a Catalyst for Advancing Micro LED

-

2024 Micro LED Commercial Developments Summary

-

Three Core Features Underpinning the Technological Value of Micro LED

-

First Key to Micro LED Commercialization: Niche Markets

-

Second Key to Micro LED Commercialization: Sensor Integration

-

Third Key to Micro LED Commercialization: Non-display Markets

-

Chapter VI. Micro LED Manufacturer Dynamic Updates

2024 Micro LED Manufacturer Capacity Analysis

-

Aixtron

-

PlayNitride

-

AUO

-

Tianma

-

Vistar

-

Future Development of AR Optical Engine Technology

-

Snap

-

SONY Raise Standards for Micro OLED Specifications

-

Meta Quest 3s

-

Meta Orion AR Defining a New Technological Benchmark for NED

-

Raysolve

-

JBD

If you would like to know more details , please contact: