TrendForce’s latest report, “2025 Micro LED Display and Non-Display Application Market Analysis”, reveals that the current development of Micro LED technology in the display sector focuses on two key challenges: optimizing manufacturing costs through design and production improvements, and identifying unique niche markets.

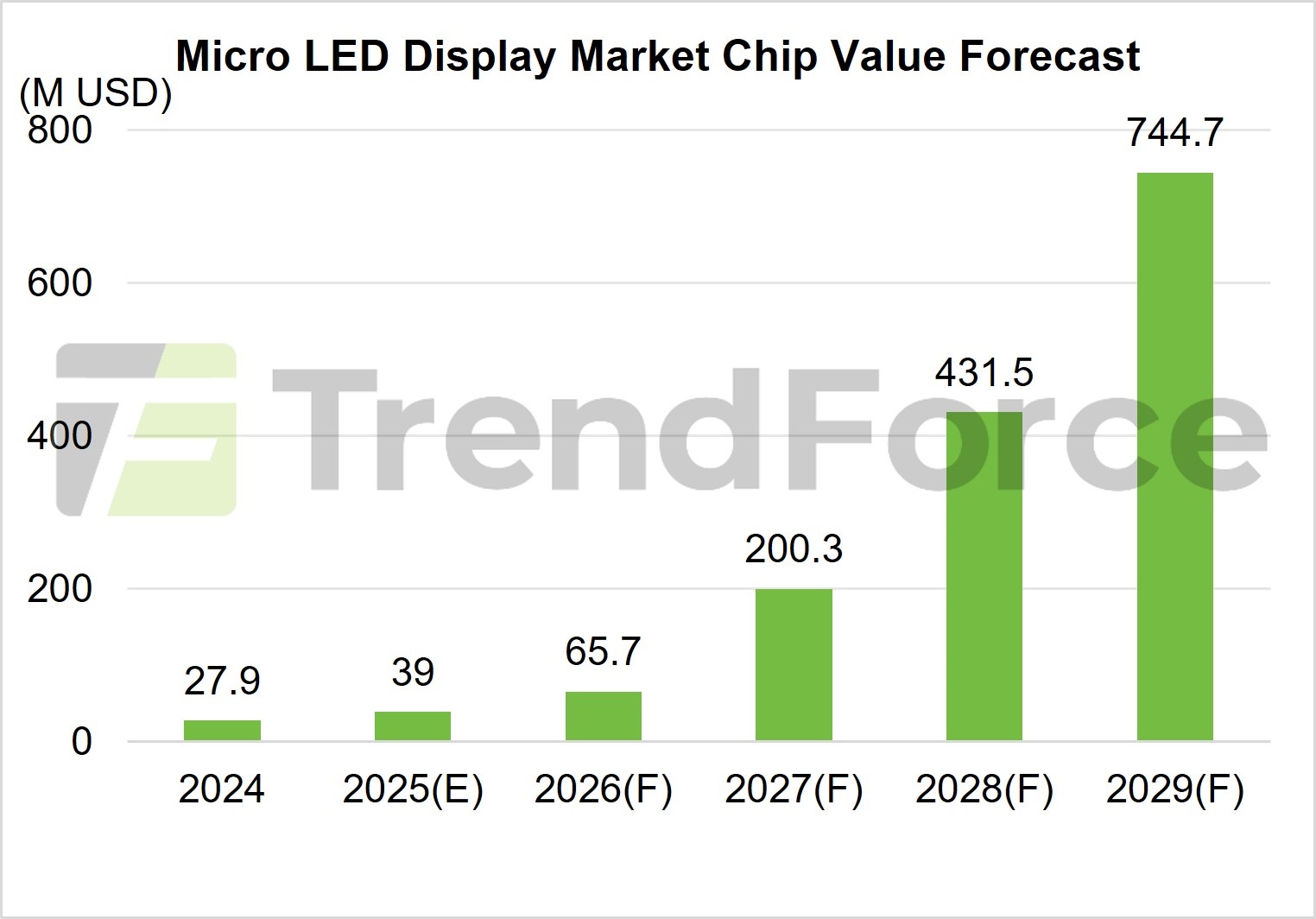

TrendForce forecasts that the chip market value for Micro LED display applications will reach US$740 million by 2029, with a CAGR of 93% from 2024 to 2029.

Cost improvements continue for large-sized displays

Presently, the bulk of Micro LED’s display-related market value is driven by large-sized displays, where Samsung holds a leading position. Future growth will rely not only on breakthrough across several critical manufacturing processes but also on collaborations between Chinese chipmakers and brand manufacturers to push chip miniaturization. This will further enhance cost advantages for mass-produced Micro LED large-sized displays.

Additionally, as AI broadens the application scenarios for head-mounted devices and as smart driving ecosystems drive up demand for advanced automotive displays, these two sectors are expected to become major pillars of Micro LED display market value in the years ahead.

TrendForce notes that the industry standard for Micro LED large-sized displays is typically 4K resolution or higher; however, the currently commercialized, mass-producible pixel pitch remains at 0.5 mm. Continued efforts to reduce pixel pitch are essential to further differentiate Micro LED from Mini LED video wall , along with overcoming challenges like low yield rates in driver connections and issues with panel seams.

Cost optimization is also shifting toward the backplane, where simplifying the manufacturing process can improve yields, and reducing the number of seams can cut down assembly steps. This contributes to overall cost reductions.

Micro LED’s standout characteristics—high brightness, high contrast, and high transparency—continue to attract investment from manufacturers. These features enable Micro LED to integrate into transparent displays for automotive windows or as part of AR-HUD or P-HUD systems, meeting the growing demand for seamless integration of virtual and real-world information for drivers and passengers. Additionally, combining Micro LED with silicon substrates offers a robust solution for near-eye displays in AR glasses, positioning Micro LED as a benchmark for next-generation metaverse-focused head-mounted devices.

Transparent displays hold great promise; non-display applications open new doors

Micro LED technology also shows strong potential in transparent display applications. These can be categorized into direct-view and micro-projection systems, with the key differences lying in viewing angels and focal distance management. In terms of use case, transparent direct-view displays are better suited for public environments where content is viewed by multiple people, and Micro LED’s combination of high brightness and high transparency makes it an ideal technology.

Meanwhile, micro-projection systems hold greater promise in privacy-sensitive personal electronic devices, where Micro LED offers ultra-miniaturized light engine solutions and is seen as the best option for micro-display technology in AR applications. Overall, Micro LED has significant room for expansion across diverse transparent display segments by developing both TFT and CMOS backplane platforms.

TrendForce emphasizes that the immediate priority for the Micro LED industry is to scale up the market quickly in order to realize economic efficiencies. As a result, non-display sectors have increasingly become important avenues for growth in addition to focusing on display applications.

These non-display opportunities span a wide range, including optical communication applications accelerated by AI, biotechnology-related medical uses, and industrial production areas such as 3D printing and photopolymerization. Ongoing innovations in these areas are adding further momentum to Micro LED’s market expansion.

Author: Thea, Eric / TrendForce

TrendForce 2025 Micro LED Display and Non-Display Application Market Analysis

Release: 29 May / 30 November 2025

Languages: Traditional Chinese / English

Format: PDF

Page: 119

Chapter I. Micro LED Display Market Analysis

-

2025-2029 Micro LED Market Value Analysis-Large-sized Displays

-

2025-2029 Micro LED Market Value Analysis-Wearable Displays

-

2025-2029 Micro LED Market Value Analysis-Head-mounted Devices

-

2025-2029 Micro LED Market Value Analysis-Automotive Displays

-

2025-2029 Micro LED Market Value Analysis

-

2025-2029 Micro LED Wafer Demand Analysis

Chapter II. Micro LED Technology Development

2.1 Module Enlargement

-

Micro LED Module Enlargement/Reduced Tiling

-

Enlarging Micro LED Modules Advantages (1/2) – Tiling Omitted

-

Enlarging Micro LED Modules Advantages (2/2) – Cost and Commercial Benefits

-

Relationships between Module Size and Tiling Size

-

Deciding Economic Module Size

-

Micro LED Module Enlargement Challenges

-

Micro LED Tiling: Large Modules vs. Small Modules

2.2 Tiling Display

-

Tiling Seams Technical Challenges

-

Micro LED Tiling Commercial Strategies : A Pixel Pitch Perspective

-

Lower Limit of Commercialization Size for Micro LED-tiled Displays: UHD

-

Upper Limit of Commercialization Size for Micro LED-tiled Displays: Economic Tiling

-

Most Suitable Sizes for Commercialized Large-sized Micro LED Displays

-

Glass: A Potential Competitor to Sapphire-based COC

-

Micro LED Heat Dissipation Challenges

-

Micro LED PPI Challenges

-

Manifesto for Achieving High-Efficiency Micro LED is Within Reach

-

Micro LED Industrial Trends (1/2): Towards Specialized Display

-

Micro LED Industrial Trends (2/2): Micro LED Enterprises to Focus on AR

Chapter III. Micro LED Transparent Display

-

Two Systems for See-through Displays: Direct-view and Micro display Projection

-

Key Differences between Direct-view and Projection Systems (1/2): Viewing Angle

-

Key Differences between Direct-view and Projection Systems (2/2): Focus Issues

-

Transparent Direct-View Displays Challenges : Mutually Exclusive Relationship between Vitality and Reality

-

Benchmarks between the Two Types of Transparent Displays

-

Transparent Direct-view Displays SWOT Analysis

-

Transparent Direct-view Displays across Different Applications SWOT Analysis

-

Transparent Direct-view Displays Development Trend Analysis

-

Things to Consider When Selecting Transparent Display Applications

-

Technology Principles by Different Transparent Displays

-

JDI Brings LCD Back to Transparent Display Competition

-

Transparent Display Application Cases

-

The Brightness–Transmittance Paradox in Transparent Displays

-

Micro LED Transparent Displays

-

Comparison between Different Transparent Display Technologies

-

Prices of Mass-produced Transparent Displays

Chapter V. Micro LED Manufacturer Dynamic

-

2025 Micro LED Player Capacity Analysis.

-

PlayNitride

-

Ennostar

-

HC Semitek

-

AUO

-

Innolux

-

Extremely PQ

-

Tianma

-

BOE

-

LGD

-

Samsung

-

Hisense

-

Hongshi

-

VueReal

-

Aledia

Appendix

-

Intel-Samsung Patent Sale

-

Advancing non-display Micro LED Technology Development - Avicena

If you would like to know more details , please contact: